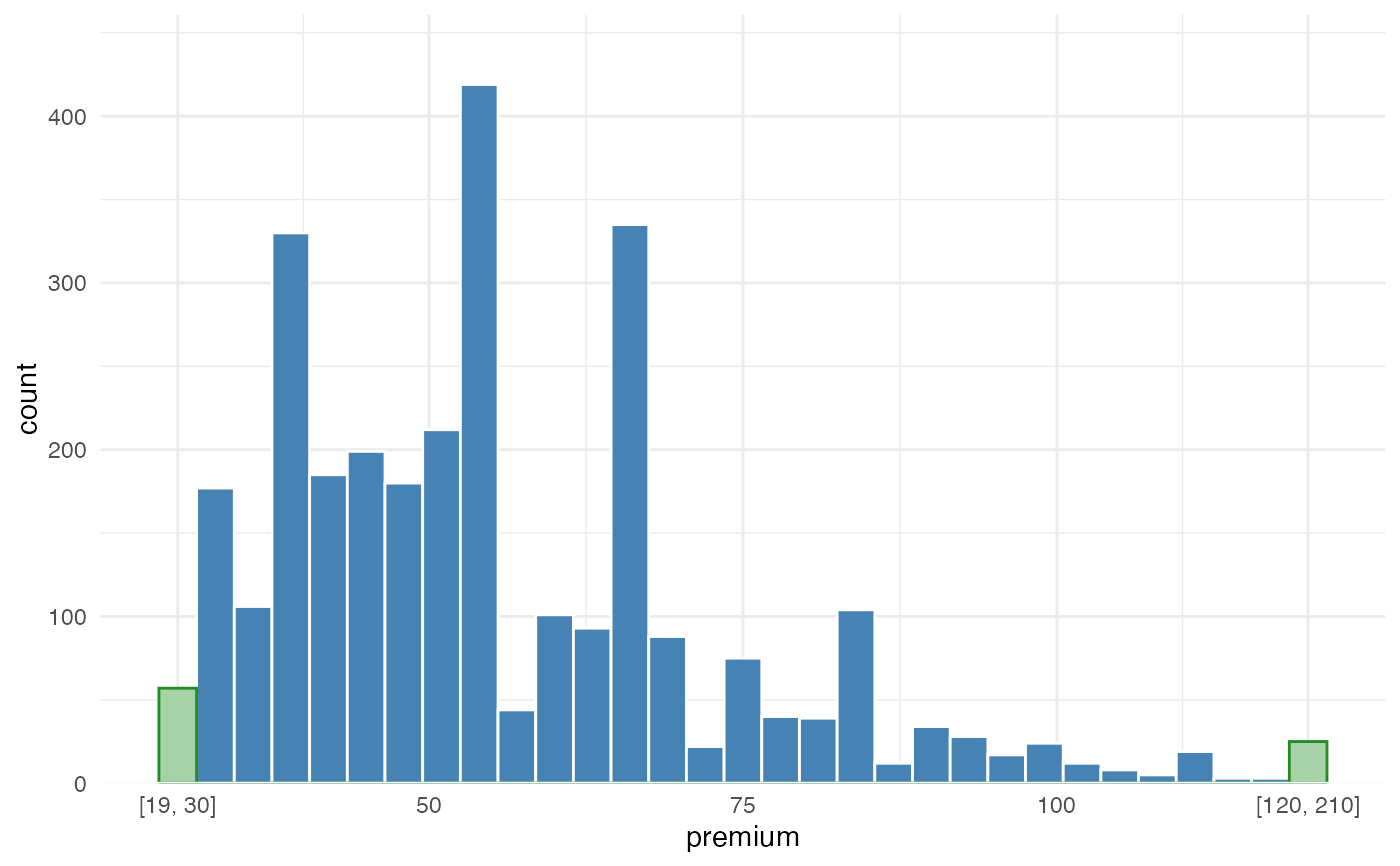

Visualize the distribution of a numeric portfolio variable while keeping extreme tails readable.

Insurance portfolios often contain skewed variables such as claim amounts,

premium, exposure, insured sums, deductibles, or fitted premiums. A few very

large policies or claim events can stretch a regular histogram so much that

the body of the portfolio becomes hard to inspect. outlier_histogram()

keeps the main range visible and groups values below lower or above upper

into dedicated tail bins.

The plot is useful for actuarial portfolio checks, data quality review, and model preparation: it helps show where most risks are concentrated while still making the presence of extreme observations explicit.

Usage

outlier_histogram(

data,

x,

lower = NULL,

upper = NULL,

density = FALSE,

bins = 30,

bar_fill = "#E6E6E6",

bar_color = "white",

tail_fill = "#F28E2B",

tail_color = "white",

density_color = "#2C7FB8",

left = NULL,

right = NULL,

line = NULL,

fill = NULL,

color = NULL,

fill_outliers = NULL

)Arguments

- data

A data.frame containing the portfolio variable to inspect.

- x

Character; numeric column in

datato plot.- lower

Optional numeric lower threshold. Values below this threshold are grouped into one left-tail bin.

- upper

Optional numeric upper threshold. Values above this threshold are grouped into one right-tail bin.

- density

Logical. If

TRUE, add a density line. Default =FALSE.- bins

Integer. Number of bins used for the displayed range. Default = 30.

- bar_fill

Fill color for regular histogram bars.

- bar_color

Border color for regular histogram bars.

- tail_fill

Fill color for tail bins.

- tail_color

Border color for tail bins.

- density_color

Color for the optional density line.

- left, right

Deprecated aliases for

lowerandupper.- line

Deprecated alias for

density.- fill, color, fill_outliers

Deprecated aliases for

bar_fill,bar_color, andtail_fill.

Value

A ggplot2::ggplot object.

Details

This function is intended as an exploratory portfolio diagnostic. It does not

remove or winsorize observations in data; it only groups tail values in the

visual display. The labels on the tail bins show the original range captured

by each tail bin.

The method for handling outlier bins is based on https://edwinth.github.io/blog/outlier-bin/.