Introduction

In many pricing analyses, model estimation is followed by a translation step.

A fitted GLM may capture the structure of the portfolio well, while some fitted effects still need to be reviewed before they are used in a tariff.

Common reasons include:

- irregular local variation

- lack of monotonicity

- externally imposed tariff structures

- expert judgement not directly represented in the model

- implementation constraints in policy administration systems

For this reason, actuarial pricing work often distinguishes between:

- model estimation

- tariff refinement

- final refit of the pricing structure

insurancerating provides a staged refinement

interface:

- fit an unrestricted model

- initialise a refinement object with

prepare_refinement() - add one or more refinement steps

- inspect these steps before refit

- call

refit()to obtain the final fitted model

This separation can make tariff adjustments easier to understand, reproduce, and audit.

When refinement can help

Refinement can help when the estimated model output is useful, but the fitted coefficient pattern needs additional structure before it is used in a tariff.

Typical use cases include:

- smoothing a rating factor derived from a continuous variable

- imposing monotonicity

- restricting coefficients to a predefined relativity structure

- introducing expert-based relativities within existing model levels

- simplifying the final tariff for practical implementation

In many workflows, refinement is applied to the model that represents the final pricing signal, such as a premium or pure-premium model. In other cases, it may also be useful for selected frequency or severity effects. The relevant question is whether the adjusted coefficient pattern is intended to support the tariff structure that will be reviewed or implemented.

Example setup

The example below starts from one common premium modelling setup:

- analyse a continuous variable with a GAM

- convert it to tariff segments

- fit frequency and severity models

- combine both into a premium proxy

- fit an unrestricted premium model

library(insurancerating)

library(dplyr)

age_policyholder_frequency <- risk_factor_gam(

data = MTPL,

claim_count = "nclaims",

risk_factor = "age_policyholder",

exposure = "exposure"

)

age_segments_freq <- derive_tariff_segments(age_policyholder_frequency)

dat <- MTPL |>

add_tariff_segments(age_segments_freq, name = "age_policyholder_freq_cat") |>

mutate(across(where(is.character), as.factor)) |>

mutate(across(where(is.factor), ~ set_reference_level(., exposure)))

freq <- glm(

nclaims ~ bm + age_policyholder_freq_cat,

offset = log(exposure),

family = poisson(),

data = dat

)

sev <- glm(

amount ~ zip,

weights = nclaims,

family = Gamma(link = "log"),

data = dat |> filter(amount > 0)

)

premium_df <- dat |>

add_prediction(freq, sev) |>

mutate(premium = pred_nclaims_freq * pred_amount_sev)

burn_unrestricted <- glm(

premium ~ zip + bm + age_policyholder_freq_cat,

weights = exposure,

family = Gamma(link = "log"),

data = premium_df

)Before refinement, inspect the unrestricted coefficient structure:

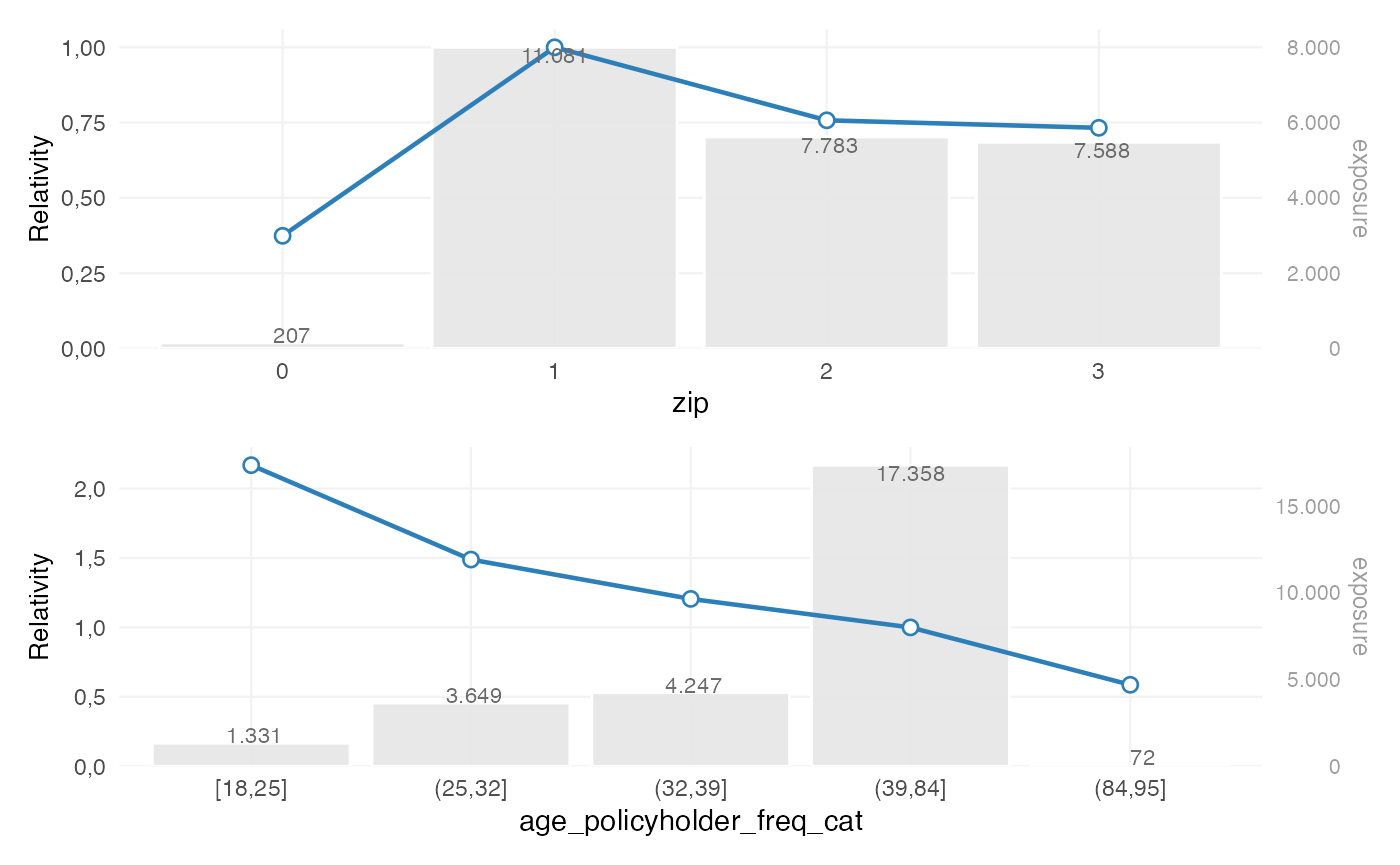

rating_table(burn_unrestricted)

#> level risk_factor est_burn_unrestricted exposure

#> 1 (Intercept) (Intercept) 1.228041e+04 NA

#> 2 0 zip 3.737317e-01 207

#> 3 1 zip 1.000000e+00 11081

#> 4 2 zip 7.574226e-01 7783

#> 5 3 zip 7.325129e-01 7588

#> 6 [18,25] age_policyholder_freq_cat 1.895596e+00 1331

#> 7 (25,32] age_policyholder_freq_cat 1.301496e+00 3649

#> 8 (32,39] age_policyholder_freq_cat 1.053848e+00 4247

#> 9 (39,51] age_policyholder_freq_cat 1.000000e+00 7421

#> 10 (51,58] age_policyholder_freq_cat 8.491823e-01 3245

#> 11 (58,65] age_policyholder_freq_cat 7.258652e-01 2791

#> 12 (65,84] age_policyholder_freq_cat 7.584714e-01 3901

#> 13 (84,95] age_policyholder_freq_cat 5.131699e-01 72

#> 14 bm bm 9.980551e-01 NA

rating_table(burn_unrestricted) |>

autoplot()

At this stage, the coefficients reflect the unrestricted model fit. This output is often informative by itself. If the pattern is too irregular, too granular or difficult to explain, a refinement step can be added explicitly.

The refinement object

Refinement begins with:

ref <- prepare_refinement(burn_unrestricted)

ref

#> <rating_refinement>

#> Base model: glm, lm

#> Steps: 0A rating_refinement object stores:

- the fitted base model

- the underlying model data

- the refinement steps added through the refinement interface

At this point, the model itself has not been refitted. The refinement object represents a proposed tariff adjustment structure, not yet the final fitted result.

This distinction is useful because refinement steps can be inspected before they are incorporated into the final model.

Smoothing

Purpose

Smoothing can be used when a rating factor derived from a continuous variable contains local variation that is hard to justify in a tariff.

For example, a coefficient pattern such as:

- age 30–34 lower

- age 34–38 higher

- age 38–42 lower again

may be statistically possible, but difficult to explain or maintain. Smoothing adds a more stable structure to the rating factor.

Adding smoothing

ref <- ref |>

add_smoothing(

model_variable = "age_policyholder_freq_cat",

source_variable = "age_policyholder",

breaks = seq(18, 95, 5),

weights = "exposure"

)The key arguments are:

-

model_variable: the grouped variable present in the GLM -

source_variable: the original continuous portfolio variable -

breaks: the preferred commercial cut points -

smoothing: the smoothing specification -

weights: optional weighting, typically exposure

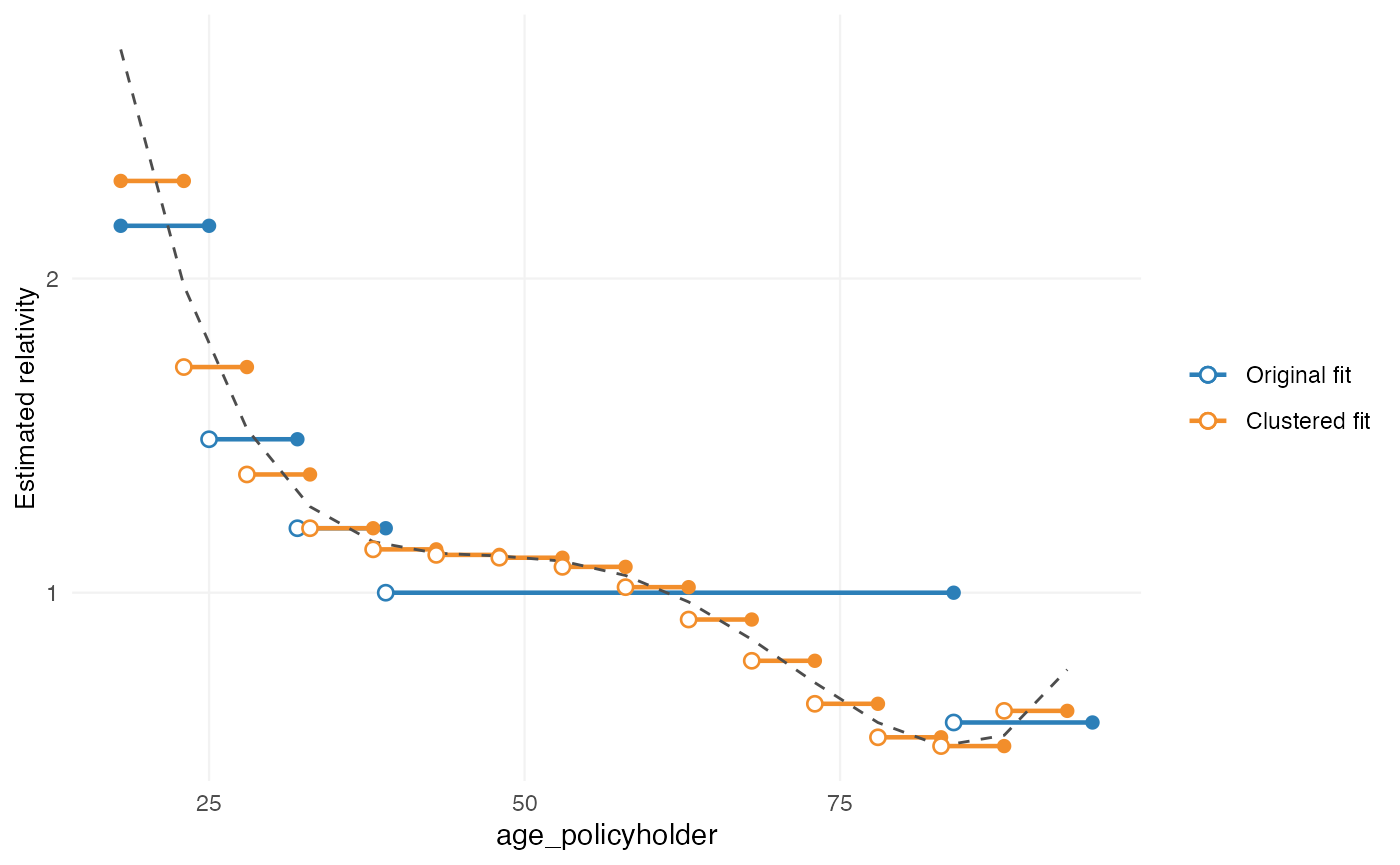

Inspecting smoothing before refit

print(ref)

#> <rating_refinement>

#> Base model: glm, lm

#> Steps: 1

#> 1. smoothing [age_policyholder_freq_cat]

autoplot(ref, variable = "age_policyholder_freq_cat")

This plot belongs to the pre-refit stage. It shows:

- the original fitted coefficients

- the proposed smoothed structure

The purpose is to inspect the refinement step itself, before it is incorporated into the final fitted model.

Choosing a smoothing method

Typical smoothing choices are:

-

"spline": polynomial-style smoothing -

"gam": flexible smooth curve -

"mpi": monotone increasing -

"mpd": monotone decreasing

The appropriate choice depends on the pricing context.

For example:

- age may justify a flexible smooth

- insured value or power may require a monotonic relationship

- low-exposure tails may benefit from exposure weighting

Restrictions

Purpose

Restrictions can be used when coefficients need to follow a predefined structure.

Typical examples include:

- bonus-malus systems

- governance-approved relativities

- externally mandated tariff structures

- implementation constraints in policy systems

Restrictions differ from smoothing:

- smoothing reshapes the fitted pattern

- restriction imposes user-defined coefficients

Adding restrictions

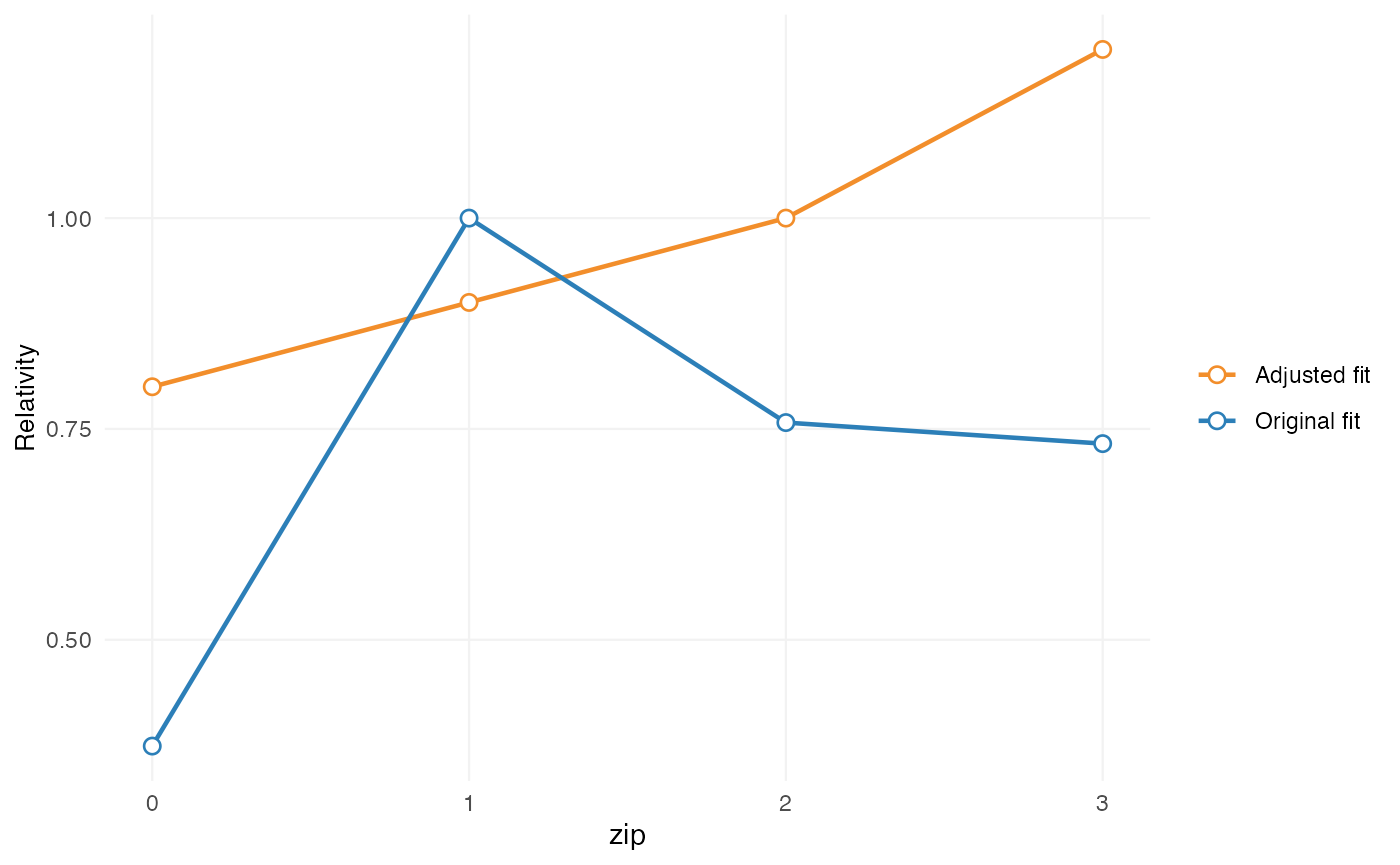

zip_df <- data.frame(

zip = c(0, 1, 2, 3),

zip_adj = c(0.8, 0.9, 1.0, 1.2)

)

ref <- ref |>

add_restriction(restrictions = zip_df)The restriction table must contain exactly two columns:

- the original factor levels

- the adjusted coefficients

Inspecting restrictions before refit

autoplot(ref, variable = "zip")

This shows the proposed restricted structure relative to the original fitted model.

Expert-based relativities

Purpose

In some cases, the fitted model uses a broad factor level, while portfolio or business knowledge suggests that more granular differentiation may be useful.

For example, a model may estimate one coefficient for “construction”, while pricing practice distinguishes between:

- residential construction

- commercial construction

- civil engineering

This can be relevant when subgroup exposure is too limited to estimate stable coefficients directly.

Adding relativities

relativities_activity <- relativities(

split_level(

"construction",

c("residential_construction", "commercial_construction"),

c(1.00, 1.15)

)

)

ref <- ref |>

add_relativities(

model_variable = "business_activity",

split_variable = "business_activity_split",

relativities = relativities_activity,

exposure = "exposure",

normalize = TRUE

)If normalize = TRUE, the relativities are scaled so that

their exposure-weighted average remains equal to 1 within the original

level.

This preserves the original model signal while introducing finer structure.

Refit

Why refit is required

Refinement steps alter part of the model structure. Once these changes are applied, the remaining coefficients may also adjust.

For that reason, the sequence does not end with

add_smoothing() or add_restriction(). The

final step is:

burn_refined <- refit(ref)This refits the model while incorporating the documented refinement steps.

Inspecting the final fitted result

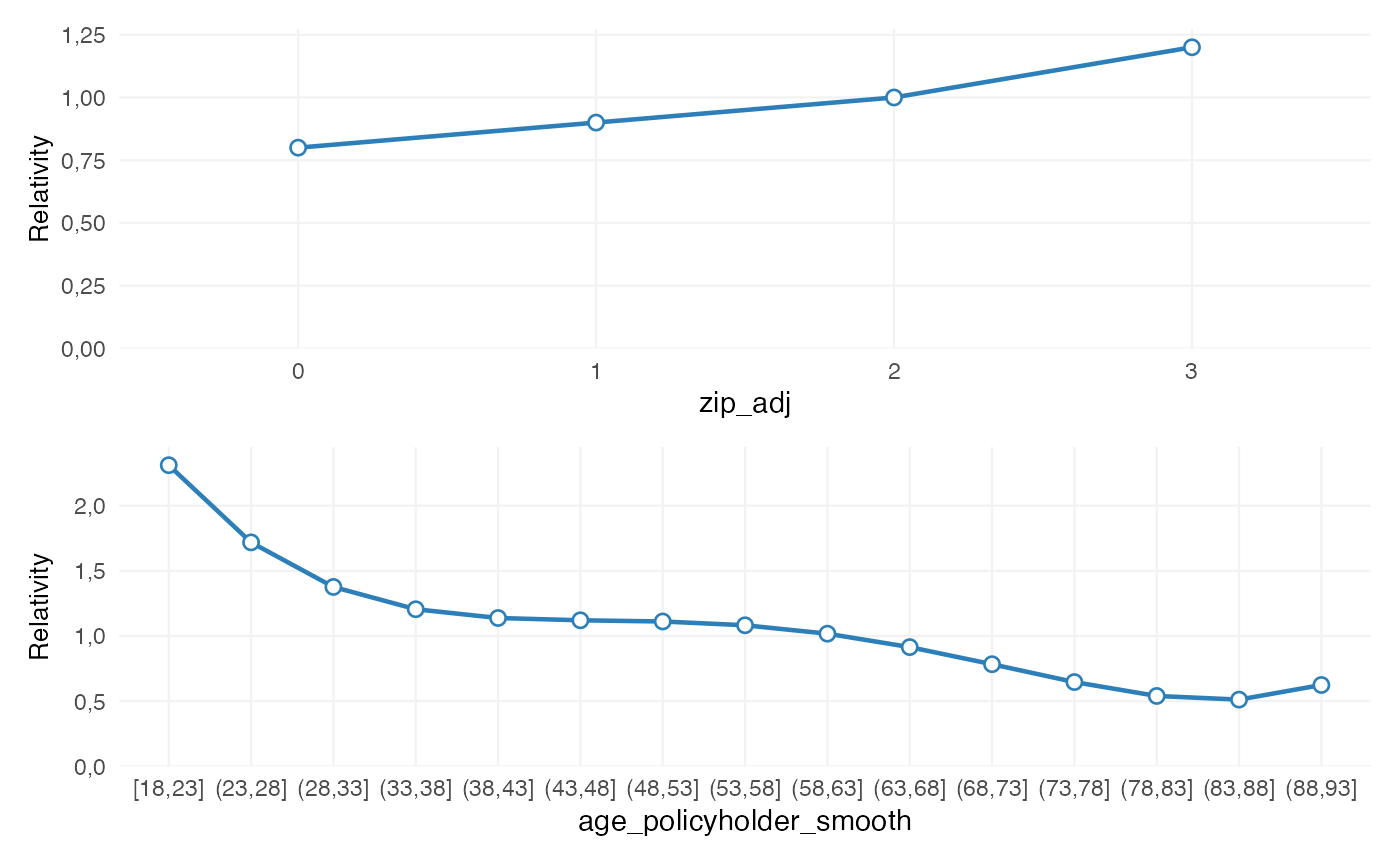

After refit, use rating_table():

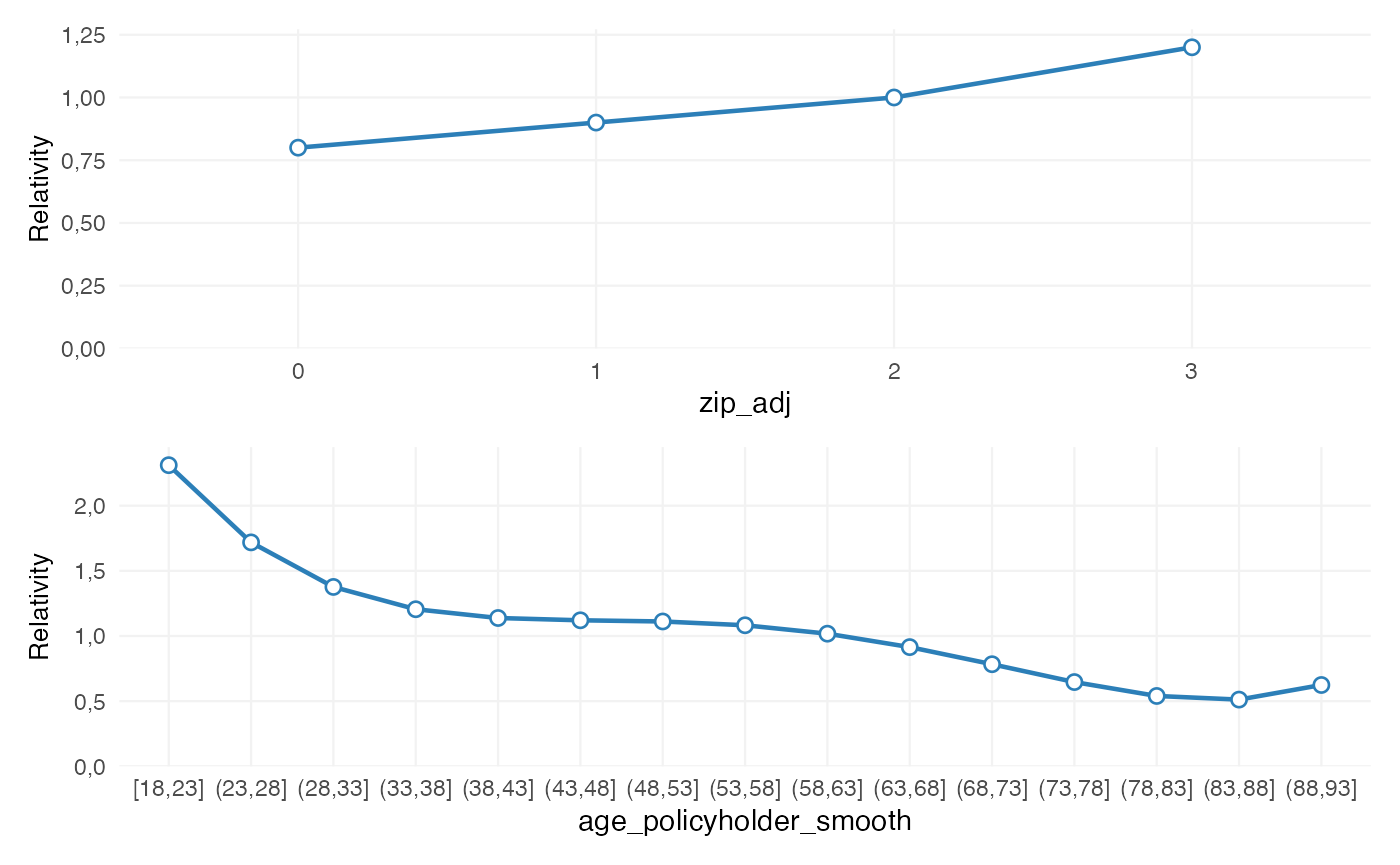

rating_table(burn_refined)

#> level risk_factor est_burn_refined exposure

#> 1 (Intercept) (Intercept) 1.070848e+04 NA

#> 2 0 zip_adj 8.000000e-01 207

#> 3 1 zip_adj 9.000000e-01 11081

#> 4 2 zip_adj 1.000000e+00 7783

#> 5 3 zip_adj 1.200000e+00 7586

#> 6 [18,23] age_policyholder_smooth 1.985214e+00 586

#> 7 (23,28] age_policyholder_smooth 1.524645e+00 2204

#> 8 (28,33] age_policyholder_smooth 1.193787e+00 2790

#> 9 (33,38] age_policyholder_smooth 1.053848e+00 3021

#> 10 (38,43] age_policyholder_smooth 1.020715e+00 3089

#> 11 (43,48] age_policyholder_smooth 9.959711e-01 3041

#> 12 (48,53] age_policyholder_smooth 9.290435e-01 2978

#> 13 (53,58] age_policyholder_smooth 8.282178e-01 2186

#> 14 (58,63] age_policyholder_smooth 7.382691e-01 1974

#> 15 (63,68] age_policyholder_smooth 7.024490e-01 1973

#> 16 (68,73] age_policyholder_smooth 7.265697e-01 1558

#> 17 (73,78] age_policyholder_smooth 7.629301e-01 907

#> 18 (78,83] age_policyholder_smooth 7.318230e-01 246

#> 19 (83,88] age_policyholder_smooth 5.983689e-01 93

#> 20 (88,93] age_policyholder_smooth 5.224158e-01 11

#> 21 bm bm 9.977213e-01 NAAt this point, the output no longer represents a proposed refinement plan. It represents the fitted coefficient structure after refinement.

The distinction is:

If smoothing, restrictions, and relativities have been applied, they are now embedded in the fitted model output.

Model data and rating grids

After refit, model structure can be extracted with

extract_model_data():

md <- extract_model_data(burn_refined)

head(md)

#> age_policyholder age_policyholder_freq_cat_smooth age_policyholder_smooth

#> 1 18 1.985214 [18,23]

#> 2 18 1.985214 [18,23]

#> 3 18 1.985214 [18,23]

#> 4 18 1.985214 [18,23]

#> 5 19 1.985214 [18,23]

#> 6 19 1.985214 [18,23]

#> nclaims exposure amount power bm zip age_policyholder_freq_cat

#> 1 1 1.00000000 261777 40 3 3 [18,25]

#> 2 0 0.09589041 0 68 5 2 [18,25]

#> 3 0 0.18630137 0 37 3 2 [18,25]

#> 4 0 0.18904110 0 33 1 2 [18,25]

#> 5 0 1.00000000 0 47 6 3 [18,25]

#> 6 1 0.06849315 6642 68 1 3 [18,25]

#> pred_nclaims_freq pred_amount_sev premium zip_adj

#> 1 0.26210773 68671.20 17999.251 1.2

#> 2 0.02502713 70854.51 1773.285 1.0

#> 3 0.04883103 70854.51 3459.898 1.0

#> 4 0.04975996 70854.51 3525.718 1.0

#> 5 0.26044368 68671.20 17884.979 1.2

#> 6 0.01802897 68671.20 1238.071 1.2Observed model-point combinations can be obtained with

rating_grid():

grid <- rating_grid(burn_refined)

head(grid)

#> age_policyholder_smooth zip bm count exposure zip_adj

#> 1 (23,28] 1 1 414 342.578082 0.9

#> 2 (23,28] 1 4 26 22.315068 0.9

#> 3 (23,28] 0 4 1 1.000000 0.8

#> 4 (23,28] 0 1 7 5.268493 0.8

#> 5 (23,28] 1 7 33 28.334247 0.9

#> 6 (23,28] 2 13 5 4.041096 1.0

#> age_policyholder_freq_cat_smooth

#> 1 1.524645

#> 2 1.524645

#> 3 1.524645

#> 4 1.524645

#> 5 1.524645

#> 6 1.524645This is typically used for:

- tariff review

- portfolio summaries

- compact prediction input

- implementation support

Complete example

One possible refinement sequence is:

zip_df <- data.frame(

zip = c(0, 1, 2, 3),

zip_adj = c(0.8, 0.9, 1.0, 1.2)

)

burn_refined <- prepare_refinement(burn_unrestricted) |>

add_smoothing(

model_variable = "age_policyholder_freq_cat",

source_variable = "age_policyholder",

breaks = seq(18, 95, 5),

weights = "exposure"

) |>

add_restriction(zip_df) |>

refit()

rating_table(burn_refined)

#> level risk_factor est_burn_refined exposure

#> 1 (Intercept) (Intercept) 1.070848e+04 NA

#> 2 0 zip_adj 8.000000e-01 207

#> 3 1 zip_adj 9.000000e-01 11081

#> 4 2 zip_adj 1.000000e+00 7783

#> 5 3 zip_adj 1.200000e+00 7586

#> 6 [18,23] age_policyholder_smooth 1.985214e+00 586

#> 7 (23,28] age_policyholder_smooth 1.524645e+00 2204

#> 8 (28,33] age_policyholder_smooth 1.193787e+00 2790

#> 9 (33,38] age_policyholder_smooth 1.053848e+00 3021

#> 10 (38,43] age_policyholder_smooth 1.020715e+00 3089

#> 11 (43,48] age_policyholder_smooth 9.959711e-01 3041

#> 12 (48,53] age_policyholder_smooth 9.290435e-01 2978

#> 13 (53,58] age_policyholder_smooth 8.282178e-01 2186

#> 14 (58,63] age_policyholder_smooth 7.382691e-01 1974

#> 15 (63,68] age_policyholder_smooth 7.024490e-01 1973

#> 16 (68,73] age_policyholder_smooth 7.265697e-01 1558

#> 17 (73,78] age_policyholder_smooth 7.629301e-01 907

#> 18 (78,83] age_policyholder_smooth 7.318230e-01 246

#> 19 (83,88] age_policyholder_smooth 5.983689e-01 93

#> 20 (88,93] age_policyholder_smooth 5.224158e-01 11

#> 21 bm bm 9.977213e-01 NA

rating_table(burn_refined) |>

autoplot()

Legacy interface

Legacy entry points remain available:

burn_refined_old <- burn_unrestricted |>

smooth_coef(

x_cut = "age_policyholder_freq_man",

x_org = "age_policyholder",

breaks = seq(18, 95, 5)

) |>

restrict_coef(zip_df) |>

refit_glm()These are primarily maintained for backward compatibility.

For new code, the recommended interface is:

This keeps the sequence of tariff adjustments explicit.

Summary

The refinement interface helps separate:

- model estimation

- tariff adjustments

- final fitted output

This makes it easier to document and inspect adjustments before the model is refitted. In practice, this can support tariff structures that are:

- statistically grounded

- interpretable

- commercially usable

- easier to implement